In recent years, the hotel sector has internalised and accepted a number of statements about OTAs that are imprecise at best, if not completely false. These “urban myths” prevent us from seeing reality as it is and in many cases cause us to make the wrong decisions.

They can be heard in debates, industry forums and interviews. All of them have some justification to them but also a much bigger false part, like all half truths.

1. “Sales from OTAs are more efficient than direct sales”

This is the original concept behind the value of OTAs and is an elegant way of saying “selling online is complicated, it requires know-how, time and a lot of money, so if you do it for yourself it will be expensive. Let us take care of it in exchange for a commission, which will be cheaper than if you do it on your own.”

- This is true when we talk about new guests who do not know your hotel. Attracting new clients to your hotel (to then gain their loyalty) is the most difficult and expensive part for a hotel or chain, and the direct channel suffers a lot in these cases as it is necessary to invest in generic marketing or other actions in order to reach the target audience. Channeling this new client through your website can be much more expensive than doing it through an OTA. We’re not saying that it’s impossible, but it isn’t easy and it usually isn’t very profitable.

- However, it is false when it comes to existing customers or those who find you on a metasearch engine, Google or any billboard other than the OTA’s own channel. Channeling guests who are

already looking for you by your name or brand (repeat customers, recommended by a friend, found on Tripadvisor, etc.) is much more expensive (and therefore less efficient) via an OTA than channeling them directly.

It would be fair to pay the OTA a very high commission for new sales and a very low commission for existing sales, but this exercise in transparency does not interest them, and they prefer to mix it up and pretend to be a much more important channel than they really are.

Let’s specify three related arguments where OTAs must be defended:

- Direct selling is neither easy nor cheap.

- Hoteliers often forget the many “hidden” costs that direct sales entail, making them believe that their cost is lower than it really is.

- For certain establishments, especially modest ones, the effort required for direct sales does not balance out, so it should not be their priority.

But despite these three arguments, in the vast majority of cases direct sales are undoubtedly much more efficient than the sale by OTAs.

2. “Booking.com is my best customer”

Booking.com selling a lot and being “your main channel” is very different from “Booking.com being your best customer”. In fact, they have little to do with one another.

Only part of the sales channeled through Booking.com counts as “new sales” for your hotel, a “new sale” referring to any customer who did not know your hotel and finds it thanks to Booking.com. A good part of your sales comes from other non-direct means, that is, ads in Google Ads (for your brand) or bids in metasearch engines (also for your brand) plus affiliate sales. How can be Booking.com your client for all these sales generated elsewhere?

Even with sales generated on their own platform, it is worth remembering that OTAs are a great marketplace with numerous levers within your reach that can help you position your product in order to reach the largest number of guests. They are fundamental billboard for making your hotel known to the world. However, it is debatable whether a reservation made on Booking.com converts Booking.com, and not the guest, into your client. Hotels that have this view forget that the real customer checks in and sleeps at their hotel for several days. What feeds the false myth that “Booking.com is my best client” is the hotel’s passivity in not creating relations with guests and converting them to full clients for all intents and purposes who try to come back and book directly.

3. “OTAs have more money: it’s difficult to compete with their deep pockets”

Their size impresses us. How can anyone suggest that direct sales can compete with OTAs given the huge difference in financial resources available, especially for marketing?

- Of course, this is true in terms of absolute financial capacity: the size of large OTA is light years away from that of the vast majority of establishments and chains. It is also true that this greater volume allows you to negotiate lower costs and therefore greater efficiency in your investments, although we have already dismissed this to a large extent in our first myth.

- It is false because the important thing is the proportional capacity, not the absolute capacity. Let’s divide the total by each expense account (each hotel), and what figure do we get? It will be equivalent to the commission that the hotels pay them.

If we accept that hotels finance OTAs and at the same time we believe that they have more money than our direct sales, then the conclusion is that we invest more in commissions than in direct sales.

4. “I can not offer a better price on my website because OTAs control me”

OTAs have traditionally limited themselves to controlling your prices in the rest of the distribution while ignoring the direct channel. This is for two main reasons:

- The direct channel is not usually a threat to the OTA (in Mirai we are working to try and make it one) and therefore they do not spend much time getting to know what happens in it.

- The fact that there is a multitude of different booking engine technologies in hotel websites makes automation (to control the price) expensive to develop and maintain. For this reason, they are limited to monitoring other OTAs, since they control thousands of hotels with a single automated technology. The classic example is Expedia, which monitors Booking.com and vice versa.

Rarely do OTAs automate price control in the direct channel and, when they do, it is because:

- The sales from your direct channel have started to be, or already are, a threat to their sales.

- Your hotel or chain is important to them (you sell a lot and they earn a lot of money with you).

Many hotels would be surprised how long it will take them to call (if they do) if they dare to put a better price on their website. Our advice is to try for yourself and see what happens.

5. “Substituting intermediated sales for direct one would mean a disaster for the hotel”

In 2016, through Skift, Expedia published a graph stating that it was not profitable for a hotel to move intermediated sales to direct sales. We disagreed at the time.

Last year, Infrata published a study funded by the ETTSA Association (whose members include large OTAs and intermediaries) in which it made an in-depth analysis of the disaster a hotel would supposedly face if it replaces its intermediated sales with direct ones.

- This is true if the statement is interpreted in the scenario that one hotel replaces all its intermediated sales. The ETTSA report took great care to define this assumption in its summary:

Were a hotel to shift their entire inventory (away from the OTA channels to Brand.com), there would be a statistically insignificant change in the overall net contribution**. This shift assumes a net cost*** rebalancing. This also assumes all other market dynamic factors remain the same. (pg 11)

However, a hotel is likely to face a significant drop in occupancy, which would require a material increase in spend in the areas of: customer acquisition, online marketing, technology development and customer services.

- It is false because nobody is posing the initial hypothesis (what would happen if a hotel moves its entire intermediated distribution to its direct sale?) Who in their right mind would ask something like that?Why not frame another question, one which is equally utopian and speculative? “what would happen if all the hotels moved their entire intermediated distribution to their direct sales”… or what would happen if a large part of the hotels moved their entire intermediated distribution to direct sales

… or what would happen if all the hotels moved a good part of their intermediated distribution to direct sales

and, above all, what we propose at Mirai: what would happen if any hotel moved a part of its intermediated distribution (the part that does not need to be intermediated and increases its direct costs) to its direct sales: would they agree to carry out that analysis?

6. “OTAs invest a lot in my hotel”

No OTA invests their money in selling your hotel. It is surprising how successful OTAs have been in making hotels believe that this myth is true. The reality is very different.

The key is to differentiate between the two types of investments that exist since the OTAs do both, hence the confusion.

- Searches by the brand or name of a specific hotel or “how the OTAs invest your money in selling your hotel”. All OTAs make announcements in your name (both in Google Ads and in meta search engines) but, even if they pay the bill, you are really the one paying for it with the sales commissions you generate. All these campaigns are negative for you because you can be present in these billboards with your direct sales. The fact that the OTAs occupy this space for you makes your direct channel sell less and your direct sales cost grow (due to the greater competition at auctions).

- Searches by destination or concept or “how OTAs invest their money to sell their brand”. We’re talking about any search that does not include a hotel name or chain. The OTAs clearly dominate here, and this money does come out of their pocket but is exclusively oriented towards positioning their brand and their points of sale, which is totally understandable. Why would an OTA advertise your hotel when searching for hotels in a destination?

7. “Without the billboard effect of the OTA, direct sales would be doomed”

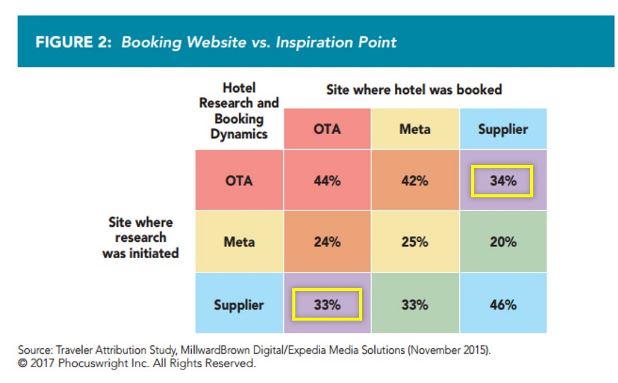

- It is true in that there is indeed an undeniable percentage of users who get to know the hotel in an OTA and end up booking directly. Studies have been published on the subject: some that have confirmed it and others that have questioned it. This is also the experience that several hotels have passed on to us: in the short term, limiting the presence in OTA reduces the number of direct reservations.

- It is false in that billboard effects exist in all directions and among all the actors. According to Saber-Phocuswright, the reverse direction is almost as extensive: customers who were inspired by hotel/chain websites but ended up booking through an OTA: There is no single dependency: all the actors are interrelated in a similar proportion.

Moreover, OTAs are in essence totally dependent on hotels for subsistence, while the opposite is debatable. If the OTAs did not exist, their traffic and influence would be transmitted to other channels. Hardly anyone would claim that customers would stop traveling. This means that its billboard effect is not only not the only one. It is not only of limited importance, it is also dispensable and fluid.

8. “There is space for all channels. Let the customer choose” (our favourite)

Who could object to giving the choice to the client? What’s wrong with freedom? Why limit options when everything could coexist in free competition? Wouldn’t it be more efficient to collaborate instead of battling each other?

Why does Mirai recommend hotels limit the presence of OTAs in meta search engines, in Google results or limit channels?

- It is true because different channels offer different value propositions. We agree on the positive aspect of presenting the maximum number of alternatives to the client and leaving the decision in their hands.

- It is false because different channels in different billboards also incur different costs for the hotel, as is normal. What Mirai proposes is that the lower final price can be transferred to the customer who chooses a channel with lower cost. OTAs do not like the idea: they have resisted price parity for legal purposes and put pressure on hotels to have the best price.

There will be no real competition and transparency while OTAs try to restrict and regulate an essential element of the market, such as price. Of course freedom of choice also includes the customer’s freedom to choose channels-billboards with a lower cost and this presumably leads to a lower price, usually in the direct channel.

Conclusion

Nobody is questioning the idea the OTAs contribute value and are essential tools for online marketing. But that does not stop many of the comments on the benefits of OTAs from being too generous, if not false. To assume these myths as true is an indication that something is wrong. The hotel sector should take a more critical look at the value proposal offered by OTAs and question each of their proposals in order to keep all the good parts that they contribute while fighting to retain the parts they take away.